The start of a new financial year is more than a calendar reset — it is an accounting reset. Therefore, preparing accurate opening balances is essential. For SMEs and startups, preparing an accurate opening balance sheet for FY 2026–27 is essential for financial clarity, compliance, and growth planning, often supported by professional accounting services.

As a result, an incorrect opening balance can distort profits, mislead stakeholders, and ultimately create tax and audit complications.

This guide explains how to prepare an opening balance sheet, key adjustments, year-end accounting checklist, and common mistakes SMEs must avoid.

Strong accounting at the beginning of the year prevents confusion at the end.

NOTICE FOR CORPORATE ENTITIES

Due date for filing of MSME Form MSME-1 for the period (Oct 2025 to Mar2026) is 30th April 2026.

Specified companies must file MSME-1 where:

- Goods or services are received from MSMEs, and

- Payments to such MSMEs exceed 45 days from the date of acceptance (or deemed acceptance)

The return must include reasons for delay in payment.

Non-compliance under Section 405 may attract:

- ₹20,000 penalty on company

- ₹20,000 penalty on officer in default

- ₹1,000 per day for continuing default

Maximum penalty up to ₹3,00,000

Quick Answer: How to Prepare Opening Balance Sheet for FY 2026–27

In short, follow these 5 steps:

- Finalise FY 2025–26 books of accounts

- Verify trial balance accuracy

- Reconcile bank, GST, debtors & creditors

- Pass closing entries & audit adjustments

- Carry forward balances to April 1, 2026

This structure helps your business maintain accurate financial reporting and compliance from day one, especially when guided by financial advisory experts.

Quick Tip

Always complete reconciliations and adjustments before carrying forward balances — never fix errors after the new financial year begins.

What Is an Opening Balance Sheet?

An opening balance sheet is the financial position of your business on the first day of the new financial year — April 1, 2026.

It reflects:

- Closing balances from FY 2025–26

- Assets and liabilities carried forward

- Updated capital accounts

- Adjustments after audit (if any)

Quick Tip

Opening Balance (FY 2026–27) = Closing Balance (FY 2025–26) + Adjustments

This is the foundation of your balance sheet format for FY 2026–27 and ensures continuity in accounting records.

Why Your Opening Balance Sheet Matters for SMEs

Many businesses ignore proper year-end accounting and opening balance adjustments — which can lead to serious financial errors.

1. Opening Balance Sheet Ensures Accurate Profit Calculation

Wrong opening balances affect revenue and expense tracking throughout the year.

2. Opening Balance Sheet Helps GST & Tax Reconciliation

Proper carry-forward ensures correct input tax credit (ITC) and liability tracking, often aligned with GST compliance processes.

3. Investor & Loan Readiness

Clean books improve credibility for funding and bank approvals.

4. Smooth Audit Process

Auditors always verify opening balances first, making audit & assurance services crucial.

Key Takeaway

Accurate opening balances are the foundation of reliable financial reporting, tax compliance, and decision-making throughout the year.

Step-by-Step Guide: Preparing Opening Balance Sheet for FY 2026–27

Step 1: Finalise FY 2025–26 Closing Entries

Before preparing your opening balance:

- First, pass all closing entries in accounting.

- Then, record all outstanding expenses and income.

- Post depreciation entries

- Close revenue and expense accounts

- Complete GST and TDS adjustments

This is a critical part of your year-end accounting checklist and often requires direct tax compliance support.

Step 2: Verify Trial Balance Accuracy

Run your trial balance and check:

- Total debits = total credits

- No abnormal or negative balances

- Suspense accounts are cleared

- Capital account is accurate

Important Note

Even a small mismatch in the trial balance can cascade into major reporting errors across the entire financial year 2026–27.

Step 3: Reconcile Key Ledgers

In other words, reconciliation ensures your books match actual records.

- Bank Reconciliation

- Debtors & Creditors Outstanding

- GST Ledger (Input vs Output)

- Loans & Interest Calculations

This step is essential for accurate opening balance journal entries and aligns with compliance best practices.

Step 4: Pass Audit Adjustments

If your accounts are audited:

- Incorporate auditor adjustments

- Update provisions and depreciation

- Correct classification errors

Only after this should balances be carried forward with support from audit professionals.

Step 5: Carry Forward Opening Balances (April 1, 2026)

Transfer balances into the new year:

| Category | Treatment |

| Assets | Carried forward at adjusted value |

| Liabilities | Same outstanding balances |

| Capital | Updated net position |

| Retained Earnings | Profit/Loss transferred |

This creates your opening balance sheet format for FY 2026–27.

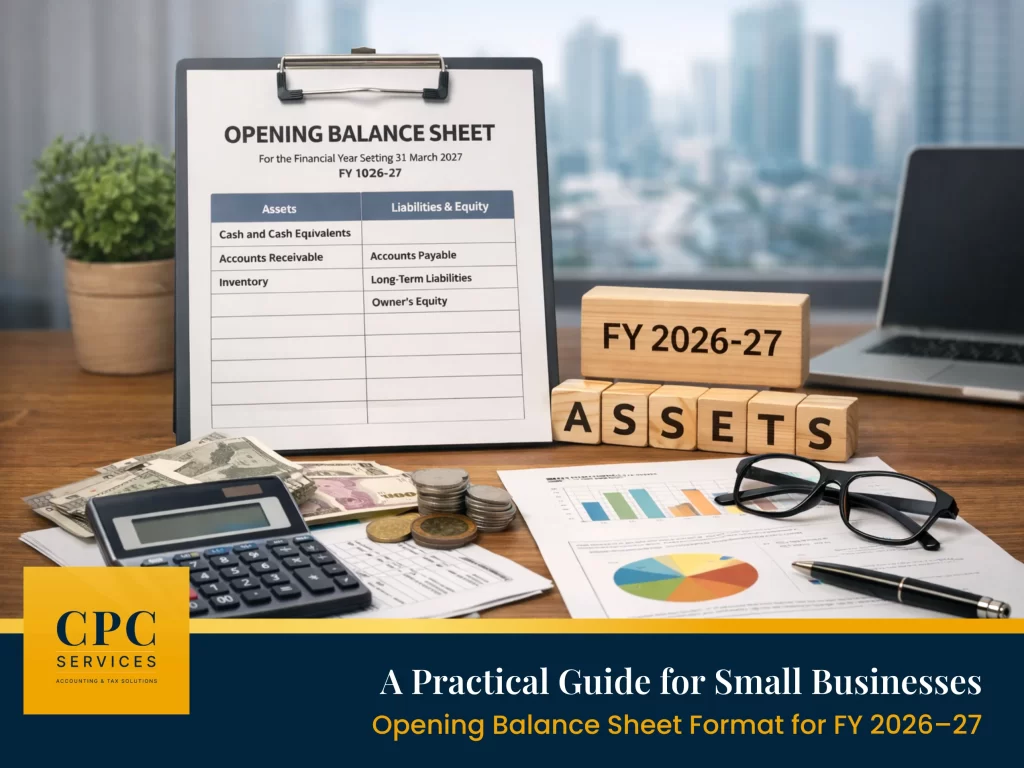

Opening Balance Sheet Format (Simple Structure)

Assets:

- Cash & Bank Balance

- Accounts Receivable

- Inventory

- Fixed Assets

- Investments

Liabilities:

- Accounts Payable

- Loans

- GST Payable

- Statutory Dues

Equity:

- Capital

- Retained Earnings

Total Assets = Liabilities + Equity

(Golden Rule of Accounting)

Example: Opening Balance Adjustment

Suppose a startup had:

- ₹10,00,000 receivables

- ₹2,00,000 unpaid expenses

- ₹50,000 depreciation missed

Without adjustment:

- Profits will be overstated

- Opening balance will be incorrect

After adjustment:

- Financials become accurate

- Tax liability is correctly calculated

CPC INSIGHT

This is why opening balance adjustments are critical for SMEs and startups.

SME Tips for a Clean Opening Balance Sheet

1. Use Accounting Software Correctly

Ensure proper year-end closure before new entries.

2. Lock Previous Financial Year

Avoid backdated errors.

3. Clean Outstanding Receivables

April is the best time for follow-ups.

4. Create Compliance Calendar

Track:

- GST due dates

- TDS return filing

- ROC filings

- Advance tax

5. Separate Personal & Business Transactions

Common startup mistake that complicates books.

Clean opening balances create clean monthly reporting and can be efficiently managed using structured accounting systems.

Common Mistakes in Opening Balance Sheet Preparation

Avoid these errors: For Example

- Carrying forward incorrect GST balances

- Similarly, missing depreciation entries can cause compounding errors.

- Ignoring unpaid expenses

- Leaving suspense accounts unresolved

- Not doing bank reconciliation

- Skipping audit adjustments

These mistakes can impact your entire financial year reporting.

CPC Insight

Many SMEs skip reconciliation and carry forward balances directly, leading to compounding errors in GST, debtors, and financial statements.

Why Startups Need an Accurate Opening Balance Sheet

For startups, your opening balance sheet FY 2026–27 is critical for:

- Monthly MIS reporting

- Burn rate analysis

- Investor reporting

- Valuation discussions

- Compliance accuracy

Poor opening balances can directly affect funding decisions, especially across various industries and business sectors.

Why Review Your Opening Balance Sheet with a Professional

Even if bookkeeping is internal, expert review ensures:

- Accurate carry-forward balances

- Proper classification of accounts

- GST reconciliation accuracy

- Clean audit trail

- Reduced compliance risk

Best Practice

Conduct a structured financial review at the start of every year with accounting and advisory experts to ensure clean books and compliance readiness.

A small review now can prevent major financial errors later. You can connect with experts here for a quick review.

Final Thoughts

Preparing an accurate opening balance sheet for FY 2026–27 is not just an accounting task — it is the financial foundation of your year.

When done correctly:

As a result, reports are reliable. Furthermore, taxes are accurate and compliance becomes easier.

The quality of your financial year depends on how well you begin it.

Need Help with Opening Balance Sheet Preparation?

If your SME or startup requires support with year-end accounting and closing entries, opening balance reconciliation, GST adjustments, compliance, or a detailed bookkeeping review, CPC Services Pvt. Ltd. can help you start FY 2026–27 with clarity, accuracy, and complete confidence.

Get your books reviewed before April 1 to avoid costly mistakes and ensure a smooth financial year ahead.